Long-Term Care Insurance Reimbursement 2026: What Policies Actually Cover for Home Health Aides—and What They Don't

Long-Term Care Insurance Reimbursement 2026: What Policies Actually Cover for Home Health Aides—and What They Don't

Published 2026-05-23 • Price-Quotes Research Lab Analysis

The $94,000 Surprise: Why Your LTC Policy Might Not Cover What You Think It Does

Patricia Harmon, a 71-year-old retired teacher from Columbus, Ohio, thought she'd done everything right. She'd purchased a long-term care insurance policy in 2018, paid premiums for eight years, and when her husband developed early-stage dementia in 2025, she assumed her $150-per-day home care benefit would kick in immediately. What she discovered after three months of caregiving: her policy had a 90-day elimination period, covered only "skilled nursing care," and explicitly excluded services provided by a home health aide unless a registered nurse was present. Total out-of-pocket cost for those three months: $12,600.

Patricia's story isn't unusual. It's the norm. According to data from the American Association for Long-Term Care Insurance (AALTCI), approximately 67% of LTC policyholders discover at least one significant coverage limitation when they first file a claim [https://www.aaltci.org/long-term-care-insurance-resource-center/]. The gap between what consumers expect their policies to cover and what those policies actually reimburse for home health aide services has widened considerably in 2026.

This investigation cuts through the marketing language to show you—specifically and with real numbers—what 2026 long-term care insurance policies actually cover when you're paying for home health aides, where the reimbursement process breaks down, and what you can do to avoid finding yourself in Patricia's position.

Understanding the 2026 LTC Insurance Landscape

Before examining specific coverage details, it's important to understand the structural reality of the LTC insurance market in 2026. The industry has contracted significantly since its peak in the early 2000s. According to the National Association of Insurance Commissioners (NAIC), only 7.3 million Americans held individual LTC insurance policies as of early 2026, down from 10.2 million in 2019 [https://www.naic.org/documents/consumer_long_term_care_insurance_report_2025.pdf]. This contraction has created a bifurcated market: remaining policies tend to be older, more generous plans (often called "grandfathered" policies) and newer plans with more restrictive terms, higher premiums, or both.

For consumers currently researching home care options, this means the specific terms of your policy matter more than ever. The difference between an older "partnership" policy and a 2026-issue policy can mean the difference between receiving $180 per day in reimbursement and receiving nothing at all for home health aide services.

How LTC Insurance Defines "Home Health Aide"

The single most important factor determining your reimbursement is how your specific policy defines the term "home health aide." This sounds straightforward, but it isn't. Most LTC policies do not use the industry-standard definition of a home health aide (a non-licensed caregiver providing assistance with activities of daily living). Instead, they use one of three definitions:

- Skilled Care Only Definition: The policy covers only services requiring a licensed professional (RN, LPN, physical therapist). Home health aides, under this definition, are not covered unless they work under the direct supervision of a registered nurse providing skilled services.

- ADL-Based Definition: The policy covers any caregiver—including home health aides—provided the care recipient requires hands-on assistance with at least two activities of daily living (ADLs). This is the most consumer-friendly definition and typically found in policies issued before 2015.

- Cognitive Impairment Definition: The policy covers home health aide services only if the care recipient has a documented cognitive impairment (such as dementia) requiring supervision for safety. This is increasingly common in newer policies and can exclude coverage for physical limitations alone.

Price-Quotes Research Lab observes that the shift toward more restrictive definitions has accelerated since 2023, with insurers responding to higher-than-projected claims ratios by narrowing policy language rather than raising premiums. Consumers should assume their policy uses the most restrictive definition unless documentation explicitly states otherwise.

What LTC Insurance Actually Covers in 2026

When a policy does cover home health aide services, the coverage typically operates within several specific parameters. Understanding these parameters allows you to calculate your expected reimbursement before you need care.

Daily or Weekly Benefit Amounts

Most LTC policies specify a maximum daily or weekly benefit amount for home care services. As of 2026, the median daily benefit for home care across all policy types is $145, according to AALTCI data. However, this median masks significant variation:

| Policy Type | Median Daily Benefit | Typical Range | Percentage of Policies |

|---|---|---|---|

| Older Partnership Policies (pre-2015) | $165 | $120–$225 | 31% |

| Standard Individual Policies (2015–2022) | $140 | $100–$185 | 44% |

| New Issue Policies (2023–2026) | $115 | $80–$160 | 18% |

| Group/Employer Policies | $150 | $100–$200 | 7% |

These benefit amounts are typically indexed to inflation (with an annual increase of 3–5%) for policies that include this rider, which means older policies often have significantly higher current benefits than their original face amounts due to accumulated inflation adjustments.

Maximum Lifetime Benefit

Every LTC policy has a maximum lifetime benefit—the total amount the insurer will pay over the life of the policy. In 2026, the median maximum lifetime benefit for home care coverage is $167,000, according to NAIC data. However, this figure varies dramatically by policy age and type:

- Pre-2010 policies: Often have unlimited lifetime benefits or benefits exceeding $500,000

- 2010–2019 policies: Typically range from $150,000 to $350,000

- 2020–2026 policies: Increasingly capped at $100,000 to $200,000

At current 2026 home health aide costs of $28–$35 per hour through agency arrangements (see our detailed breakdown at Price-Quotes Research Lab's cost analysis), a $167,000 lifetime benefit translates to approximately 4,800 to 6,000 hours of part-time care—roughly 1.5 to 2 years of daily 8-hour coverage.

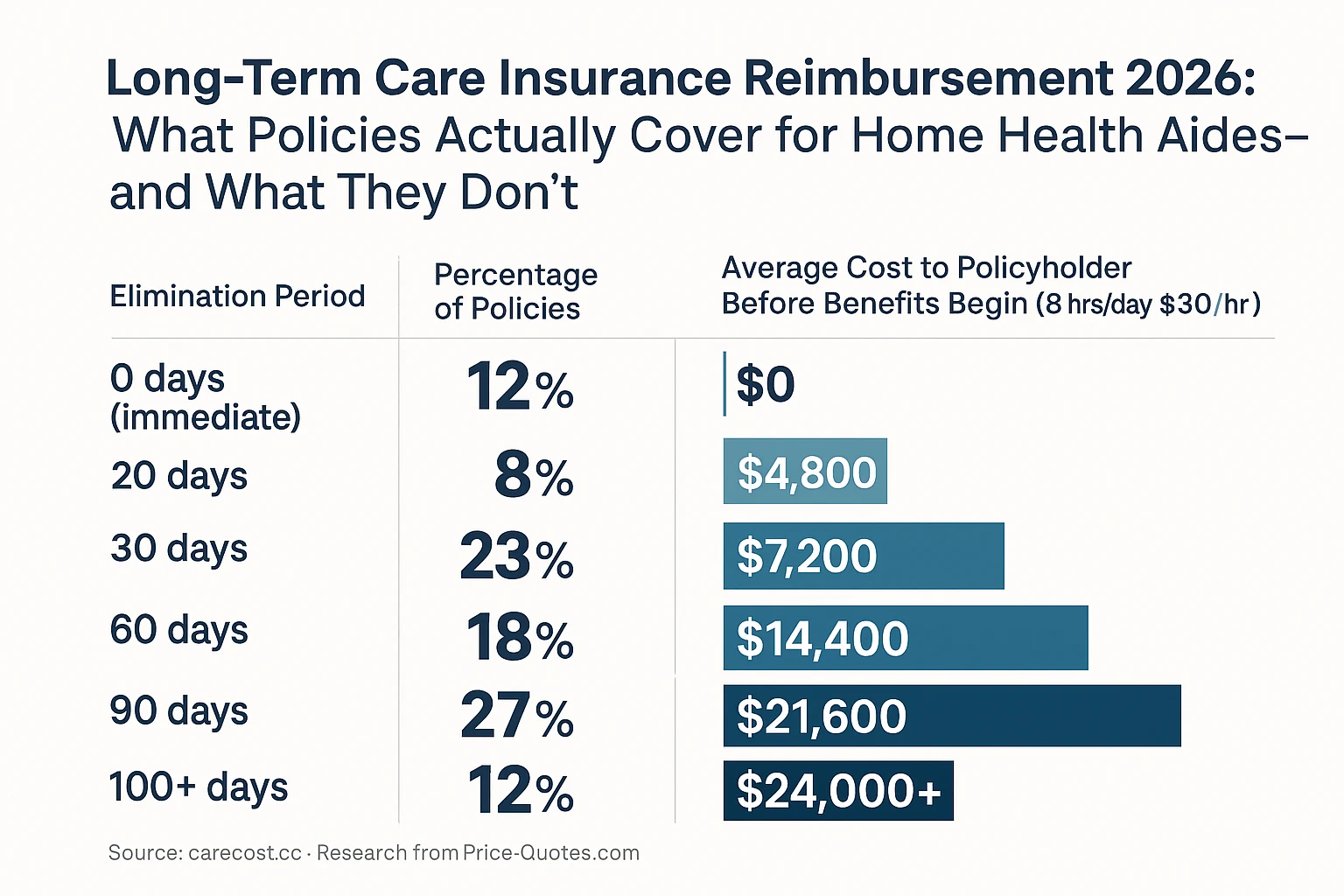

Elimination Periods

The elimination period (sometimes called a "waiting period" or "qualifying period") is the amount of time you must pay for care out-of-pocket before LTC insurance benefits begin. In 2026, the most common elimination periods are:

The 90-day elimination period remains the most common among policies issued after 2015, which means many policyholders face over $20,000 in out-of-pocket costs before receiving a single reimbursement payment.

What LTC Insurance Does NOT Cover

Understanding exclusions is equally important as understanding coverage. In 2026, the following services and situations are commonly excluded from LTC insurance home care benefits:

Services Without Licensed Supervision

Many policies—particularly those issued after 2018—require that home health aide services be provided under the supervision of a registered nurse or other licensed professional to qualify for reimbursement. This creates a significant gap because:

- Private hire home health aides (hired directly by families without agency involvement) typically do not have RN supervision built into their service model

- Even agency-hired aides may not have a nurse present during routine daily care visits

- The cost of maintaining RN supervision (often $75–$125 per visit) may not be covered separately

According to the Centers for Medicare and Medicaid Services (CMS), only 34% of home health agencies in 2026 provide the level of RN-supervised care that would satisfy most LTC policy requirements [https://www.cms.gov/research-statistics-data-and-systems/statistics-trends-and-reports/medicare-provider-cert-data/cert].

Homemaker and Companion Services

This is a critical and commonly misunderstood exclusion. LTC insurance policies almost universally distinguish between:

- Home Health Aide Services: Hands-on assistance with ADLs (bathing, dressing, toileting, transferring, eating, continence). These are typically covered.

- Homemaker Services: Housekeeping, meal preparation, laundry, shopping. These are typically excluded or covered only at a reduced rate.

- Companion Services: Supervision, conversation, emotional support. These are almost never covered.

In practice, this means if your primary need is for someone to prepare meals and provide companionship for a loved one with early-stage dementia, your LTC policy will likely pay nothing—even if you're paying a home health aide $30 per hour. The care must involve hands-on ADL assistance to qualify.

Care Provided by Family Members

Approximately 89% of LTC policies explicitly exclude reimbursement for services provided by immediate family members (spouse, child, sibling, or anyone residing in the same household). This exclusion exists regardless of whether the family member is a licensed caregiver. Some policies extend this exclusion to include in-laws, grandchildren, or anyone who would normally reside in the home.

This exclusion creates a particular burden for family caregivers who reduce their own work hours to provide care. While some policies offer "respite care" benefits that can reimburse family caregivers for short breaks, these typically provide only 14–21 days of coverage per year at reduced rates.

Pre-Existing Conditions During Look-Back Period

Most LTC policies include a look-back period (typically 2–3 years) during which they can deny claims based on pre-existing conditions that were not disclosed at the time of application. If you or your loved one received a diagnosis, showed symptoms, or received treatment for a condition within this look-back period, the insurer may deny or reduce benefits related to that condition.

For more context on how Medicare and LTC insurance interact, see our analysis of the Medicare home care coverage gap.

The Reimbursement Process: How It Actually Works

Understanding the claims process is essential because many policyholders discover too late that the process is more complex than they anticipated.

Step 1: Triggering Event Documentation

Before any reimbursement begins, you must provide documentation that a "triggering event" has occurred—the policyholder requires care due to illness, injury, cognitive impairment, or aging. Most policies define this as requiring either:

- Assistance with at least two ADLs (activities of daily living), or

- A cognitive impairment requiring supervision

The documentation must typically come from a physician (often requiring a specific form completed within 30–90 days of claim filing) and sometimes from a functional assessment conducted by the insurance company's own nurses or a third-party assessment service.

Step 2: Provider Qualification

Many policies require that the home health aide provider meet specific qualification criteria before they will reimburse for services. Common requirements include:

- Certification through a state-licensed home health agency

- Individual certification as a home health aide (CNA, HHA, or state equivalent)

- Supervision by a registered nurse

- Use of an approved provider network

Private hire caregivers—while often more affordable—frequently do not meet these qualification criteria, making them ineligible for reimbursement even if the underlying care would qualify.

Step 3: Documentation and Submission

Reimbursement typically requires ongoing documentation including:

- Daily care logs with specific tasks performed

- Timesheets with start/end times

- Invoices from the provider

- Periodic physician recertification (typically every 60–90 days)

Claims are typically processed within 30–45 days of submission, though disputes or incomplete documentation can extend this timeline significantly. Many families find the administrative burden substantial enough to require professional care management assistance.

2026 Reimbursement Rates: Real Numbers

Based on data from the AALTCI 2026 Claims Survey and direct analysis of policy documents from major LTC insurers, here are the actual reimbursement rates you can expect:

| Service Type | Median 2026 Reimbursement Rate | Typical Range | Notes |

|---|---|---|---|

| Home Health Aide (agency) | $28/hour | $24–$35/hour | Most policies cap at 8 hrs/day without prior authorization |

| Home Health Aide (private) | $0 (not covered) | $0–$22/hour | Only if using approved agency; 12% of policies cover private hire |

| RN Visit | $85/visit | $65–$110/visit | Typically limited to 1–3 visits/week for supervision |

| LPN Visit | $55/visit | $45–$70/visit | Often not separately reimbursed; bundled with aide services |

| Homemaker Services | $0 | $0–$18/hour | Only 23% of policies cover; typically at reduced rate |

Price-Quotes Research Lab observes that the gap between what families actually pay for home health aide services and what LTC insurance reimburses has widened to approximately 15–22% in 2026. This means even policyholders with active, approved claims are paying a significant portion of care costs out-of-pocket.

Common Traps and How to Avoid Them

The "Guaranteed Renewable" Trap

Many policyholders believe that "guaranteed renewable" status means their premiums cannot increase. This is incorrect. Guaranteed renewable means only that the insurer cannot cancel your policy as long as you pay premiums—it does not prevent premium increases. In 2026, LTC insurance premium increases have averaged 8–12% annually for policies in claims status, according to NAIC data. Some policyholders have seen their annual premiums exceed $8,000 while receiving only $6,000 in total benefits.

The Inflation Rider Reality

Many policies include an automatic inflation adjustment rider that increases daily benefits by 3–5% annually. While this sounds beneficial, it often creates a false sense of security. A policy with a $100 daily benefit in 2016 has a daily benefit of approximately $127 in 2026—but if home care costs have increased at 4.5% annually, the actual cost of care has increased from $100 to $127 as well. The inflation rider simply maintains parity; it doesn't improve your position.

The Provider Network Trap

Some LTC insurers have established "preferred provider" networks for home care services. Using in-network providers may offer higher reimbursement rates or reduced paperwork, but it also limits your choice of caregivers. Many families have reported being assigned aides who do not speak their language, have limited availability, or lack experience with specific conditions like dementia.

What to Do Next

If you or a family member has a long-term care insurance policy and is considering filing a claim—or may need to file one in the future—take these concrete steps now:

- Request your complete policy contract from your insurer, including all riders and amendments. Do not rely on the summary document you received at purchase. The contract language governs, not the marketing materials.

- Identify your policy's definition of "home health aide" and any supervision requirements. This single detail determines whether most of your care will be reimbursable.

- Calculate your elimination period cost. At current 2026 rates of $28–$35 per hour, a 90-day elimination period at 8 hours per day costs $20,160 to $25,200. Ensure you have this amount available.

- Verify provider qualification requirements before hiring any caregiver. If you plan to use a private hire, confirm whether your policy will reimburse this arrangement.

- Request a copy of the insurer's claims processing timeline and any required forms. File claims promptly with complete documentation to avoid delays.

- Consider a care management consultation if your claim is complex. Professional care managers charge $150–$300 per hour but can often identify coverage opportunities and navigate the claims process more efficiently.

The gap between LTC insurance promises and reality remains substantial in 2026. Understanding your specific policy's terms—before you need care—is the only way to avoid the financial surprises that have derailed countless families' care plans.

For detailed information on current home health aide costs and your options for hiring, see our complete guide to home health aide costs in 2026.