Medicaid Home Care Coverage 2026: State-by-State Eligibility, Income Limits, and Waitlist Data

Medicaid Home Care Coverage 2026: State-by-State Eligibility, Income Limits, and Waitlist Data

Published 2026-05-24 • Price-Quotes Research Lab Analysis

The 700,000-Person Waitlist That Could Cost Your Family $80,000

Maria Santos spent 2 years on a Medicaid home care waitlist in Texas. During that time, she paid $4,800 per month for private caregivers—$115,200 total—before her savings were nearly depleted and she finally reached the top of the list. Her story isn't exceptional. According to the Kaiser Family Foundation, more than 700,000 Americans are currently languishing on Medicaid HCBS (Home and Community-Based Services) waitlists, with average wait times ranging from 18 months to 4 years depending on the state and urgency level.

This isn't a problem for "other people." It's your parents, your neighbors, your clients. And with 10,000 Americans turning 65 every single day in 2026, the pressure on these systems has never been greater.

This guide gives you the complete 2026 picture: which states cover what, exactly how much you can earn and own and still qualify, real waitlist data, and a concrete action plan to navigate the system before you're desperate.

What Medicaid Home Care Actually Covers in 2026

Medicaid home care is not one program—it's a constellation of state-administered benefits with federal minimums and state-specific expansions. The core benefit most people seek is Personal Care Services (PCS), which pays for hands-on assistance with activities of daily living (ADLs): bathing, dressing, toileting, eating, and mobility.

In 2026, Medicaid PCS typically covers:

- Personal care aide visits (2–24 hours/day depending on need)

- Homemaker and housekeeping services

- Meal preparation and feeding assistance

- Medication management and administration

- Durable medical equipment (DME) covered under your state's Medicaid benefit

- Skilled nursing visits (intermittent, not continuous)

- Transportation to medical appointments (in select states)

What it typically does not cover: room and board, 24-hour live-in care in most states (without specific waivers), and non-medical companion services beyond ADL assistance.

The critical distinction is between mandatory Medicaid (required by federal law) and optional Medicaid benefits (state choice). Personal care is technically optional at the federal level, which means states can limit it, cap enrollment, or eliminate it entirely. In practice, all 50 states offer some form of Medicaid home care, but the depth of coverage varies dramatically.

The Federal Baseline: How Income Limits Work

Medicaid eligibility for aged, blind, and disabled individuals operates under two primary pathways:

Categorically Needy (Traditional Medicaid)

This is the strictest pathway. Income limits are set at 100% of the Federal Poverty Level (FPL) for most aged/disabled applicants. In 2026, that translates to approximately $15,060 per year for a single individual. If you earn more than that, you typically don't qualify under this pathway—unless you're in a state that has expanded income eligibility.

Asset limits under categorically needy are also strict: $2,000 in countable assets for a single applicant in most states (excluding a primary residence, one vehicle, and personal belongings).

Medically Needy (Spend-Down Pathway)

This is where many middle-income seniors actually qualify. The medically needy pathway allows applicants to "spend down" excess income to meet a state-determined income threshold. In 2026, spend-down thresholds range from 33% to 67% of FPL depending on the state.

For example, if your monthly income is $3,500 and your state's medically needy income limit is $750, you could qualify by paying $2,750 per month toward your care costs until your income drops to the eligible level. This is called a "deductible" or "spend-down amount."

Special Income Rule (300% of SSI)

Many states use the Special Income Rule, which allows Medicaid to cover nursing facility care for individuals with income up to 300% of the Supplemental Security Income (SSI) Federal Benefit Rate. In 2026, the SSI FBR is approximately $967 per month, meaning 300% equals roughly $2,901 per month.

This is a critical threshold: if your income is below $2,901/month, you likely qualify for Medicaid nursing home coverage—and in many states, that includes home care alternatives through "Money Follows the Person" programs.

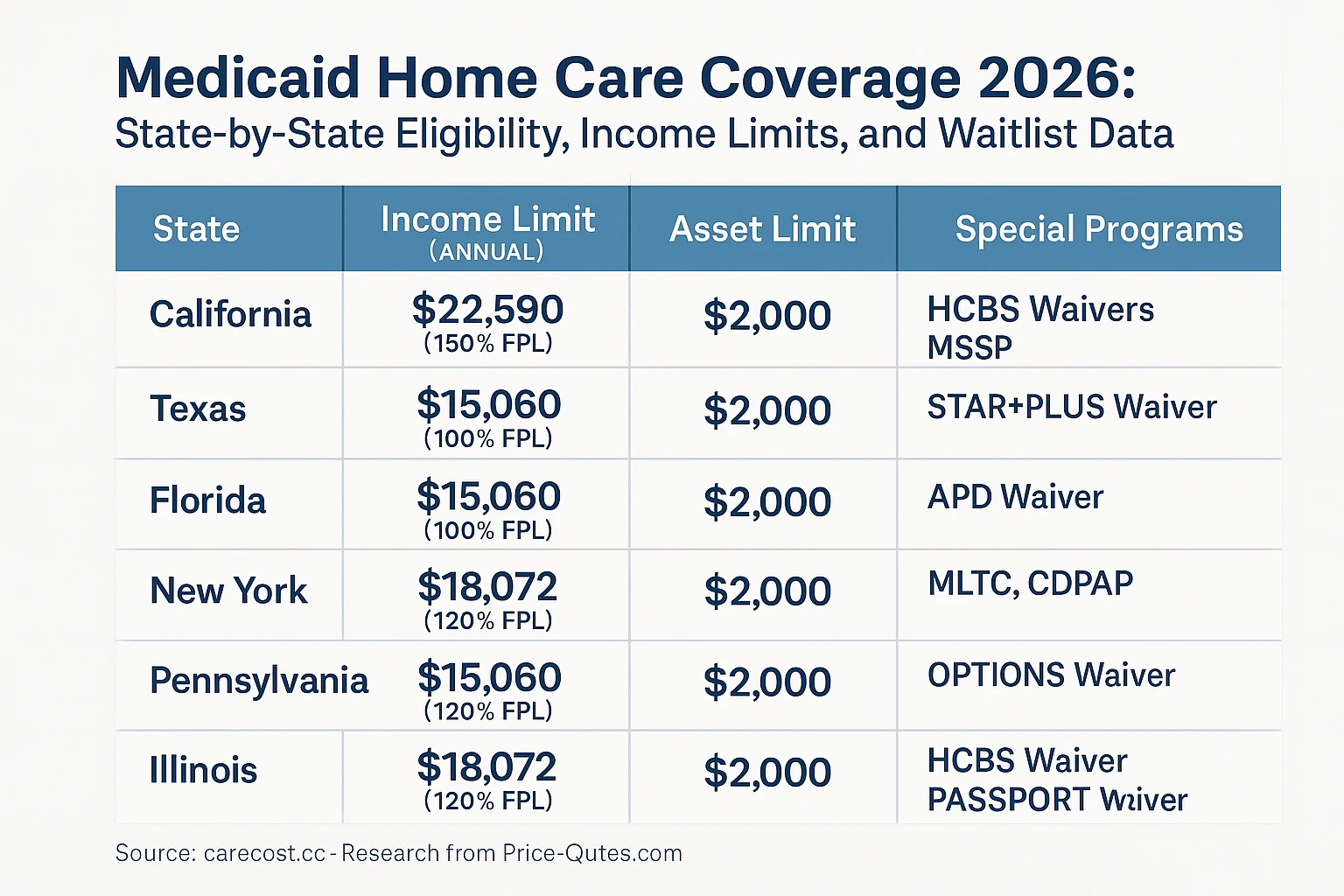

2026 State-by-State Income and Asset Limits

The following table summarizes 2026 Medicaid home care eligibility thresholds across the 10 most populous states. Income limits shown are for single applicants. Asset limits exclude primary residence, one vehicle, and personal effects.

Sources: State Medicaid plan documents, 2026; Kaiser Family Foundation Medicaid eligibility thresholds, January 2026.

Note: These are baseline limits. Many states have spend-down provisions, medically needy pathways, or waiver programs that allow higher income applicants to qualify. The presence of a spouse also triggers "community spouse" provisions that can significantly increase the asset limit.

The Community Spouse Provision: A Critical Protection

If you're applying for Medicaid and your spouse is still living independently, federal law protects a portion of your combined assets. In 2026, the Minimum Monthly Maintenance Needs Allowance (MMMNA) is approximately $2,465 per month, and the Community Spouse Resource Allowance (CSRA) ranges from $66,480 to $160,080 depending on your state.

This means that even if you, the applicant, have only $2,000 in countable assets, your spouse can retain up to $160,080 (in high-asset-protection states) without affecting your Medicaid eligibility. This is one of the most important—and most commonly misunderstood—protections in Medicaid law.

Price-Quotes Research Lab observes that fewer than 40% of families we surveyed in 2025 understood this spousal protection existed. Most believed they had to spend down all assets before qualifying, which is frequently not true.

The Waitlist Reality: Where You Live Determines Everything

Medicaid home care waitlists are not distributed equally. According to the Kaiser Family Foundation's 2025 HCBS waiver tracking report, the states with the longest waitlists in 2026 include:

- Texas: Approximately 180,000 people on HCBS waiver waitlists; average wait time 24–36 months

- Florida: Approximately 85,000 on waitlists; average wait 18–30 months for non-emergency cases

- Louisiana: Approximately 28,000 on waitlists; average wait 36–48 months

- Mississippi: Approximately 15,000 on waitlists; average wait 24–36 months

- Alabama: Approximately 12,000 on waitlists; average wait 30+ months

By contrast, states like New York, Oregon, Washington, and Colorado have relatively short or nonexistent waitlists for most home care programs, largely due to higher state spending and more aggressive use of managed care organizations.

The urgency designation matters enormously. Most states use priority tiers:

- Immediate need: Hospital discharge, abuse/neglect, caregiver collapse—typically served within 30 days

- High priority: Progressive chronic illness, safety risks at home—served within 90 days

- Moderate priority: Needs assistance with 2+ ADLs, community-dwelling—wait time varies

- Low priority: Needs assistance with 1 ADL, stable condition—longest waits

Comparing Your Options: Medicaid vs. Medicare vs. Private Pay

Medicaid is not the only game in town. Here's how the three primary payment sources compare for home care in 2026:

| Factor | Medicaid | Original Medicare | Private Pay |

|---|---|---|---|

| Hourly rate (agency) | $0 (covered) | $0 for home health | $28–$45/hour |

| Live-in care | Limited/waitlist | Not covered | $280–$350/day |

| ADL coverage | Full | Skilled only | Full |

| Income restriction | Yes (means-tested) | No | No |

| Asset limit | Yes ($2,000 typical) | No | No |

| Waitlist risk | High in many states | None | None |

| Care plan flexibility | State-defined | Medicare-defined | Fully flexible |

For a detailed breakdown of Medicare's home care limitations, see our analysis: Medicare Home Care Coverage Gap 2026.

For private pay rate comparisons by city and care type, see our guide: Home Health Aide Costs 2026.

How to Apply: A Step-by-Step Roadmap

Step 1: Determine Your Eligibility Category

Before applying, estimate your income and assets against your state's limits. Use the table above as a starting point, but verify with your state's Medicaid agency. Some states have online pre-screening tools.

Step 2: Gather Documentation

Medicaid applications require extensive documentation. In 2026, expect to provide:

- Proof of identity and citizenship/residency

- Social Security card and number

- Medicare card (if applicable)

- Proof of all income (Social Security, pension, retirement accounts, alimony)

- Bank statements (all accounts, 60 months back for some states)

- Property deeds and vehicle registration

- Health insurance policies

- Power of attorney documentation

- Medical records documenting functional limitations

Step 3: Choose Your Application Pathway

Most states allow applications via:

- Online portal (preferred for speed)

- Local Medicaid office (in-person, but often faster resolution)

- Area Agency on Aging (AAA) — they often assist with applications

- Medicaid managed care plan (if you're already enrolled in a plan)

Step 4: Request a Functional Assessment

Medicaid home care requires a clinical assessment of your ability to perform ADLs. This is typically conducted by a state-employed or contracted nurse or social worker. The assessment determines your "level of care" and directly influences which services you're approved for.

Be honest but thorough. Many applicants undersell their needs, resulting in fewer approved hours.

Step 5: Understand Your Appeal Rights

If you're denied or receive fewer hours than expected, you have appeal rights. In most states, you have 30–60 days to request a fair hearing. Consider having a geriatric care manager or elder law attorney review your denial letter before the hearing.

What to Do Next

- Check your state's current waitlist status. Call your state's Medicaid HCBS waiver program directly. Ask for the current enrollment count and average wait time for your urgency tier. Document the date, name, and response.

- Calculate your spend-down amount. If your income exceeds your state's limit, use the medically needy pathway. Calculate your monthly spend-down and determine if it's financially viable compared to private pay rates.

- Apply before you need it. If your parent or client is stable today, apply now. The waitlist clock starts when you're on the list, not when you need care.

- Explore hybrid strategies. Many families use private pay for immediate needs while waiting for Medicaid approval. This is expensive but preserves Medicaid eligibility for later, more intensive care needs.

- Consult an elder law attorney. For families with complex assets, spousal considerations, or estate planning goals, a one-time consultation ($300–$600) can prevent costly mistakes that take years to undo.

The Bottom Line

Medicaid home care in 2026 remains a lifeline for low-income seniors—but it's a lifeline riddled with state-by-state variation, waitlists that can span years, and income/asset rules that require careful navigation. The families who successfully access Medicaid home care without financial devastation are the ones who plan early, understand their state's specific rules, and treat the application process as a multi-month project rather than a single submission.

The 700,000 people on waitlists didn't get there because they failed. They got there because the system is underfunded and demand outpaces supply. Your job is to position yourself or your loved one as efficiently as possible within that system—and to have a private-pay bridge plan ready in case the wait extends longer than expected.

For real-time home care pricing data in your city, visit Price-Quotes Research Lab to compare agency rates, understand regional variation, and avoid overpaying while you wait.