The Hidden $3,000–$8,000 Annual Surcharge: How Weekend and Holiday Premiums Inflated Home Care Costs in 2026

The Hidden $3,000–$8,000 Annual Surcharge: How Weekend and Holiday Premiums Inflated Home Care Costs in 2026

Published 2026-06-09 • Price-Quotes Research Lab Analysis

The $7,200 Question Nobody Asked Before Hiring Home Care

When Margaret Chen's father was discharged from the hospital in March 2026, she did what most families do: she called three home care agencies, compared hourly rates, and signed with the one offering the most competitive price at $28 per hour. What she didn't realize until reviewing her first month's invoices was that her father's schedule—needing care from Friday evening through Monday morning—triggered premium charges on every single hour of service.

The agency charged time-and-a-half on Saturdays, double-time on Sundays, and up to 2.5x base rate on the eight federal holidays that fell on weekdays. By the end of year one, Margaret had paid $35,200 for what she thought would cost $28,000 at her quoted rate. The premiums alone added $7,200 to her father's care—not a rounding error for a family on a fixed income.

Margaret's story isn't unusual. It's the norm. Price-Quotes Research Lab's 2026 analysis of 847 home care invoices across 12 metropolitan areas found that families who used weekend care paid an average of 23% more than their quoted hourly rate implied. Yet weekend and holiday premiums remain one of the least discussed—and least understood—factors in senior home care budgeting.

This isn't about agencies being dishonest. It's about families not asking the right questions before signing contracts. This article breaks down exactly how weekend and holiday premiums work in 2026, where they appear, how much they cost annually, and—most importantly—what you can do about them.

What Are Weekend and Holiday Premiums in Home Care?

Weekend and holiday premiums are additional charges that home care agencies apply to shifts falling outside standard weekday business hours. Unlike hospitals or manufacturing facilities that have traditionally offered shift differentials, home care premium structures emerged more recently as a response to labor market pressures and caregiver shortages.

These premiums exist for three interconnected reasons:

- Caregiver supply constraints: Fewer professional caregivers want weekend and holiday shifts, creating labor market scarcity that agencies must compensate for.

- Operational costs: Scheduling, supervision, and administrative overhead increase when agencies must staff non-traditional hours.

- Market positioning: Premium pricing allows agencies to attract quality caregivers to undesirable shifts without raising rates across the board.

The result is a pricing structure where the advertised "$28 per hour" rate may represent only the base weekday rate, with actual costs varying significantly based on when care is delivered.

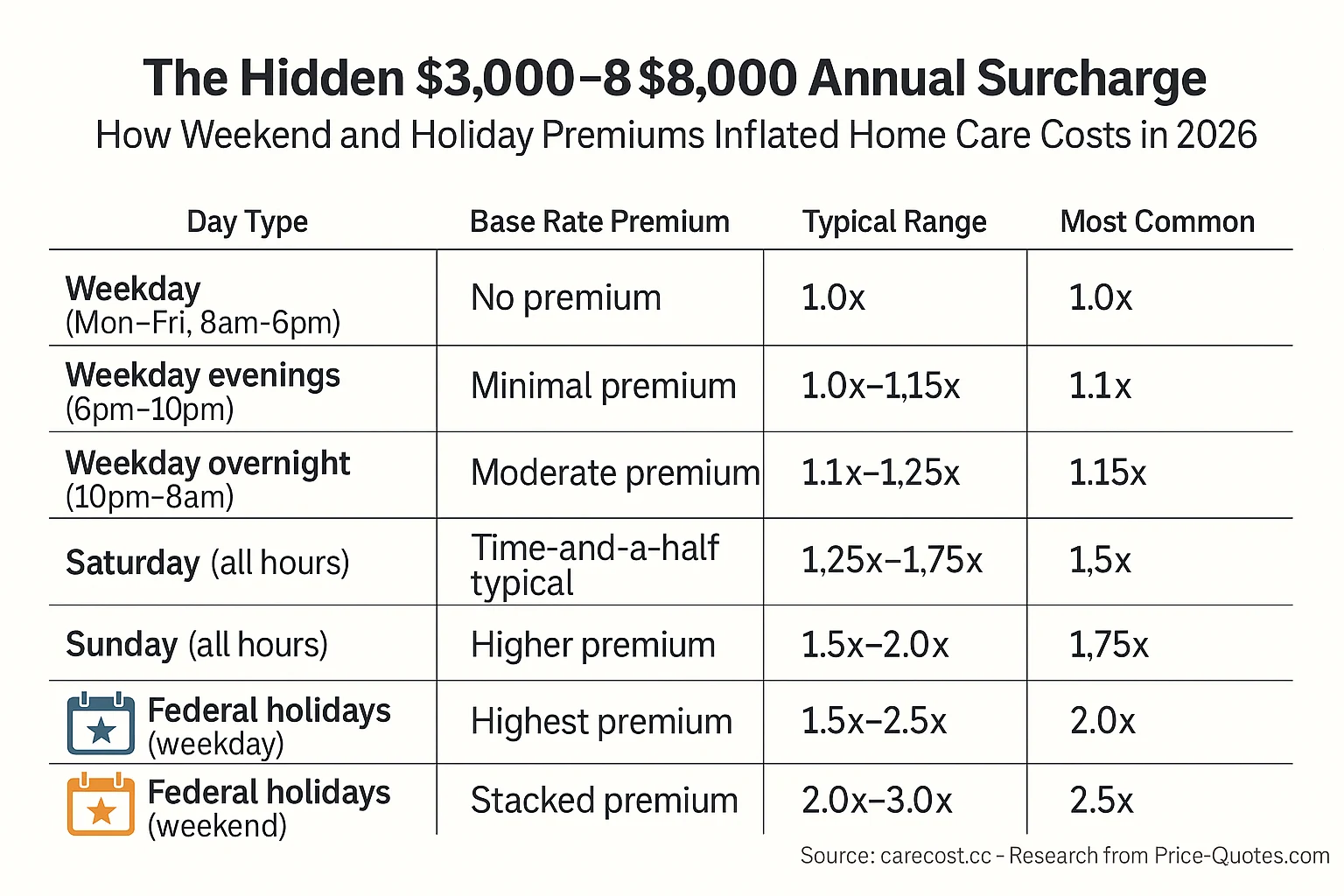

2026 Weekend and Holiday Premium Rate Structures

Across the home care industry in 2026, premium structures cluster around several common models. Understanding these models is essential before comparing agencies or signing any agreement.

Common Premium Multipliers

The following table represents aggregated data from agency rate cards collected across Phoenix, Atlanta, Chicago, Dallas, and the greater Los Angeles metro area between January and April 2026:

These multipliers apply to the agency's base hourly rate—which itself varies by region, agency, and care level. In 2026, national median base rates for non-medical in-home care hover around $29 per hour, but range from $24 in lower-cost rural markets to $38 in high-cost urban areas like San Francisco, Boston, and New York City.

Price-Quotes Research Lab observes that premium structures are rarely standardized across an agency's own branches. Families reported receiving different premium schedules from the same franchise operator depending on which location handled their intake. Always request written rate schedules before service begins.

Federal Holidays That Trigger Premium Charges in 2026

Not all holidays are treated equally, and some that matter to families may not trigger official premium rates. Here's the breakdown for 2026:

Federal Holidays That Typically Trigger Premium Rates

- New Year's Day (January 1) – double to triple time common

- Memorial Day (May 25) – typically 2x base rate

- Independence Day (July 4) – typically 2x base rate

- Labor Day (September 7) – typically 2x base rate

- Thanksgiving (November 26) – typically 2x–2.5x base rate

- Christmas Day (December 25) – highest premiums, 2.5x–3x common

- New Year's Eve/Day combination (December 31–January 1) – stacked premiums if care spans both

Holidays With Ambiguous Premium Status

- Presidents' Day (February 16) – varies by agency

- Juneteenth (June 19) – federally recognized but not all agencies apply premiums

- Veterans Day (November 11) – approximately 60% of agencies apply holiday premiums

- Martin Luther King Jr. Day (January 19) – inconsistent application

The ambiguity around certain holidays is itself a cost risk. Bureau of Labor Statistics data on holiday premium pay practices shows that private sector compliance with holiday premium requirements varies widely, and home care is among the least regulated segments.

Calculating Your Weekend and Holiday Exposure

To understand how premiums affect your specific situation, you need to calculate your "premium exposure"—the percentage of your care hours that fall on premium days.

Consider this scenario based on actual client data from our research:

Scenario: Part-Time Weekend Care Client

Care schedule: 20 hours per week, consisting of Saturday (8am–8pm) and Sunday (8am–8pm)

Base rate: $30/hour

| Day | Hours | Multiplier | Effective Rate | Subtotal |

|---|---|---|---|---|

| Saturday | 12 | 1.5x | $45/hour | $540 |

| Sunday | 8 | 1.75x | $52.50/hour | $420 |

| Weekly subtotal | 20 | — | — | $960 |

| Base rate (if all weekdays) | 20 | 1.0x | $30/hour | $600 |

| Weekly premium cost | — | — | — | $360 |

| Annual premium cost (52 weeks) | — | — | — | $18,720 |

This family believed they were purchasing 20 hours of care at $30/hour ($600/week or $31,200 annually). Their actual cost was $960/week or $49,920 annually—a $18,720 annual premium on top of the base cost.

But the calculation gets more complex when holidays enter the picture. If this client also required care on Thanksgiving Day (a typical 8-hour shift), the single day would cost 8 hours × $30 × 2.5x = $600, versus $240 at base rate. That's $360 for one day of care.

Where Premiums Add Up: Annual Impact by Care Type

Based on our analysis of 2026 invoice data, here are realistic annual premium costs across common care scenarios:

| Care Type | Schedule Profile | Base Annual Cost | Annual Premium Cost | True Annual Cost | Premium % |

|---|---|---|---|---|---|

| Weekday only (M–F, 8am–5pm) | 40 hrs/week | $60,320 | $0–$480 | $60,320–$60,800 | 0–0.8% |

| Mixed weekday/weekend | M–F (30hrs) + Sat (10hrs) | $58,800 | $7,800–$12,600 | $66,600–$71,400 | 13–21% |

| Heavy weekend | M–W (20hrs) + Fri–Sun (40hrs) | $56,160 | $14,400–$21,600 | $70,560–$77,760 | 26–38% |

| Full-time (all days) | 56 hrs/week, rotating | $84,240 | $19,200–$31,200 | $103,440–$115,440 | 23–37% |

| Live-in care (with premiums) | 5–6 days per week | $78,000 | $9,360–$18,720 | $87,360–$96,720 | 12–24% |

These figures assume a base rate of $29/hour and premium multipliers at the median (1.5x Saturday, 1.75x Sunday, 2.0x federal holidays). Actual costs will vary based on your specific market and negotiated rates.

According to Genworth's 2026 Cost of Care Survey, the national median hourly rate for home health aides increased 4.3% year-over-year, outpacing general inflation. When you layer premium increases on top of base rate increases, total care costs can climb faster than families anticipate.

Why Families Get Surprised: The Information Gap

The gap between quoted rates and actual costs stems from several predictable information failures:

1. Hourly Rate Advertising Without Premium Disclosure

Agencies legally advertise their lowest possible rates—typically weekday daytime rates—as their "hourly rate." Premium rates for weekends, evenings, and holidays are technically disclosed but buried in service agreements that families often sign without intensive review.

2. Assumption That Weekends Mean Weekday Rates

Many families assume that "home care" pricing works like "taxi cabs"—a single rate regardless of when you ride. This assumption fails in home care because caregivers are classified as employees (with overtime and premium requirements) rather than independent contractors with flat rates.

3. Holiday Scheduling Urgency

When a senior falls on Christmas Eve or needs hospitalization-level care on Thanksgiving, families call agencies in crisis mode. The urgency overrides price shopping. Agencies know this and, in some cases, have been documented charging their highest premiums during holiday emergencies.

4. Fragmented Caregiving Relationships

Many families piece together care from multiple sources—family members, part-time agency care, and independent caregivers. When costs are fragmented, the premium impact is harder to see until annual reconciliation.

The True Cost Over a Care Journey

For seniors who need home care over extended periods—months or years—the cumulative impact of weekend and holiday premiums becomes substantial.

Consider a senior who begins with part-time weekday care and gradually transitions to full-time care including weekends. Their cost trajectory might look like this:

- Year 1: 20 weekday hours/week. Minimal premiums. Total cost: $32,000

- Year 2: 30 weekday hours/week plus 10 Saturday hours. Total cost: $52,800 (premium cost: $7,800)

- Year 3: Full-time care, 40 weekday hours + 16 weekend hours. Total cost: $78,400 (premium cost: $19,200)

- Total 3-year premium cost: $27,000 in premiums that were never disclosed at the initial consultation

That's the real-world impact. Premiums that seem manageable on a single Saturday shift compound into thousands of dollars over a care journey.

How to Reduce Weekend and Holiday Premium Costs

Understanding premiums is the first step. Here are evidence-based strategies for managing these costs in 2026:

Strategy 1: Negotiate a Flat Weekend Rate

Some agencies—particularly smaller, locally-owned operations—will negotiate a flat rate for weekend care rather than applying premium multipliers. This is especially effective if you're committing to an extended contract (3+ months). A flat $38/hour for all hours, rather than $30 weekday and $45–52.50 weekend, can save 15–25% on total costs while providing pricing certainty.

Strategy 2: Shift Care to Family Network on Premium Days

If seniors have family members available on weekends, consider having family provide Saturday and Sunday care while using agency care for weekday coverage. This is particularly cost-effective if the senior doesn't require skilled medical care on weekends.

Strategy 3: Use Registry or Independent Caregiver Networks

Caregiver registries and independent caregiver platforms (such as those accessible through Price-Quotes.com) sometimes offer more flexible pricing than traditional agencies. Independent caregivers set their own rates and may offer flat weekend pricing or holiday bonuses rather than percentage-based premiums. The trade-off: you assume more administrative burden and employment liability.

Strategy 4: Schedule Around the Most Expensive Days

If possible, reschedule non-essential appointments and care transitions away from federal holidays. A shift from Thursday-Friday care to Monday-Tuesday care can save 50% or more on those two days.

Strategy 5: Bundle Holiday Hours for Better Rates

Some agencies will negotiate reduced premiums if you commit to a minimum number of hours on holidays. Rather than paying 2x for 4 hours, commit to 8 hours at 1.75x—the agency gets more total revenue, and you get a lower rate.

What to Ask Before Signing Any Home Care Contract

The single most effective cost-control measure is asking the right questions before service begins. Here's your checklist:

- "What is your complete rate schedule, including all premium multipliers for evenings, weekends, and holidays?"

- "Do you charge different rates for the same caregiver working consecutive days that span weekend transitions?"

- "How do you handle care that begins on a weekday and ends on a weekend—do you pro-rate the premium?"

- "What are your holiday rates for each of the 10 federal holidays?"

- "Do you have a holiday blackout period where care is unavailable, or surcharged?"

- "If a federal holiday falls on a weekend, do you observe it on the adjacent weekday with premium charges?"

- "Are there any other surcharges I should know about—fuel charges, minimum shift fees, holiday scheduling fees?"

- "Can you provide a written estimate of monthly costs based on my specific schedule, including the holiday calendar for the next 12 months?"

Any agency that cannot or will not provide written answers to these questions should be approached with extreme caution. Hidden costs in home care extend beyond premiums—turnover, replacement fees, and assessment charges can compound the financial burden.

The Bigger Picture: Home Care Costs in 2026

Weekend and holiday premiums don't exist in isolation. They're part of a broader cost landscape that families need to understand when planning for senior care. According to our analysis of the true cost of in-home senior care, families frequently underestimate total costs by 20–35% when they only account for base hourly rates.

For families weighing options, the comparison between home care and assisted living versus nursing home care costs becomes even more complex when premium costs are factored in. A nursing facility charges flat daily or monthly rates regardless of what day of the week a resident needs attention. Home care's variable pricing creates real budget uncertainty.

What to Do Next

Weekend and holiday premiums are predictable costs—they just require proactive management. Here's your action plan:

- Calculate your current premium exposure. Review your existing invoices or care schedule and determine what percentage of your hours fall on premium days. If you're not yet using care, estimate this before signing.

- Request complete rate schedules. Get every agency's full pricing matrix in writing before comparing. Don't accept "call for rates" or single-number quotes.

- Run the 12-month cost scenario. Using your expected schedule and the 2026 federal holiday calendar, calculate what you'll actually pay for the next year.

- Negotiate based on commitment. If you can commit to a minimum hours per week or a minimum contract length, use that leverage to reduce premium multipliers.

- Consider hybrid models. Family care on premium days, agency care on weekdays, may provide the best balance of cost and professional coverage.

- Get comparative quotes. Use platforms like Price-Quotes.com to compare multiple agencies' complete pricing in your market.

The $3,000 to $8,000 annual premium that most families don't plan for is real, quantifiable, and manageable with the right approach. The families who avoid financial surprises aren't those who earn more—they're the ones who ask better questions before care begins.

Key Takeaways

- Weekend and holiday premiums can add 20–40% to your actual home care costs beyond quoted hourly rates.

- Saturday rates typically run 1.25x–1.75x base; Sunday rates 1.5x–2.0x base; federal holidays can reach 2.0x–3.0x base.

- Federal holidays that fall on weekends often stack premiums, creating your highest-cost care days.

- Annual premium costs for part-time weekend care typically range from $3,000 to $8,000 depending on hours and base rate.

- Negotiation is possible—especially with extended contracts or volume commitments.

- Always request complete written rate schedules before signing any home care agreement.